What is an Activist Shareholder?

An “activist shareholder” is an investor who actively uses their position as a shareholder to influence corporate management, with the goal of increasing corporate value (i.e., the share price). They are also called “activists.” These activists are known to use confrontational tactics such as writing sharply worded letters to management, proxy fights seeking to oust incumbent directors, etc. Because they tend to focus on lifting the share price on short-term basis (through dividends or share buybacks), their tactics often prevent companies from making long-term investments such as Redevelopment Projects.

In Japan, domestic activists such as the Murakami Fund have been well-known, but recently overseas investment funds have also begun targeting companies with low capital efficiency.

The U.S. activist investment firm Elliott International, L.P. has recently acquired 3.51% of Sumitomo Realty & Development’s shares, rising to become the third-largest shareholder (as of January 2026). The impact that this firm may have on Sumitomo’s redevelopment projects deserves close attention going forward.

1. The Arrival of U.S. Activist Firm Elliott

Activist shareholders use their ownership to put pressure on management, often pushing for the disposal of low-return real estate or unprofitable businesses to quickly increase corporate value (i.e., the share price). Their focus tends to be on short-term profits rather than long-term returns such as those represented by redevelopment projects.

As expected, Elliott has already started making various demands to Sumitomo’s management, including requests for the sale of company-owned buildings and enhanced shareholder returns.

Because Sumitomo’s top and second largest shareholders are both trust accounts (which rarely intervene actively in management), Elliott has become the largest active shareholder challenging the company’s management.

2. Sumitomo vs. Elliott: “Oil and Water” in Terms of Redevelopment

There is reason to believe that the influence of Elliott on Sumitomo’s redevelopment business will be significant, because the two are fundamentally at odds regarding redevelopment projects.

From the perspective of U.S. activists, the main concerns are improving ROE (Return on Equity) and ROI (Return on Investment) to raise the share price through short-term profit maximization. By contrast, redevelopment projects are long-term efforts that look ahead 20 years or more, making them inherently incompatible with activists’ focus on short-term improvement.

Furthermore, long-term activities in urban redevelopment—such as early land acquisition (“land sharking”), leaving vacant houses and lots for extended periods after acquisition, etc.—are likely to be viewed as capital inefficiencies by activists.

3. Early Signs of Its Influence? Changes around Sengakuji

Recently, Sumitomo Realty temporarily halted activities in the Sengakuji area, and the timing seems to coincide with Elliott’s rise as a shareholder. This suggests a possible connection.

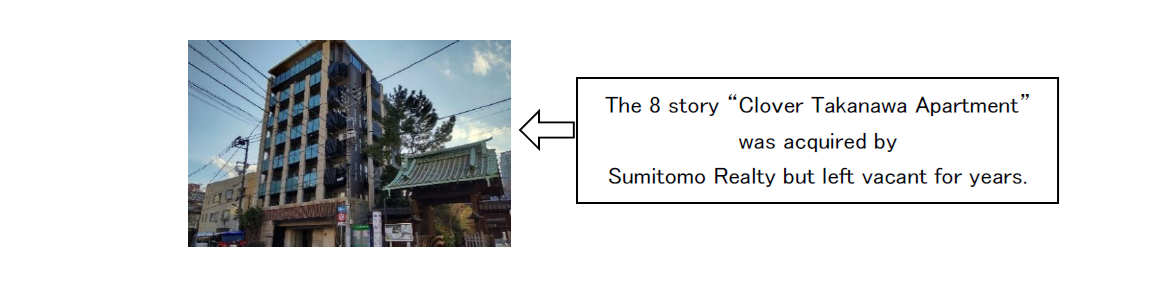

In Sengakuji, Sumitomo had been aggressively acquiring local properties, leaving a newly constructed rental apartment building “Clover Takanawa” completely vacant for a long period as if redevelopment was inevitable. However, since Elliott’s appearance, the building has started filling with tenants, which may suggest that activists’ pressure influenced the shift—because a wholly vacant building represents an unused asset that produces no revenue.

Sumitomo acquired many other units from older apartments in the area as well. However, almost all of them still remain vacant. Why? It seems they are unable to utilize their properties because of structural or seismic reasons that older apartments have. The lack of utilization demonstrates how economic rationality has been overlooked by Sumitomo in their development efforts.

4. The Many “Sumitomo Realty Buildings” Seen Around Tokyo

Driving around central Tokyo, you may notice many buildings with “Sumitomo Realty” in the name. Sumitomo has a tendency to retain completed buildings as unliquidated assets rather than selling them.

Activist shareholders like Elliott view such holdings as signs of inefficient capital use and have been calling on management to sell company-owned buildings. Even if these assets have large unrealized gains, if that value is not reflected in the stock price, activists apply pressure for sales.

Selling these buildings can generate significant profit, boost the share price, and provide funds that can be used to repay debt, increase dividends, or repurchase shares—further supporting stock price increases.

Activists can even propose replacing directors if management resists such moves—making them formidable opponents for management.

Summary

• While redevelopment projects usually require around 20 years to complete, activists emphasize short-term share price gains and shareholder returns.

• Activists view prolonged holding of vacant properties as inefficient capital allocation.To their eyes, this kind of commercial activity appears to be nothing but an“untolerable inefficient business transaction.”

• The appearance of the U.S. activist firm Elliott as Sumitomo’s third largest shareholder has already led to various proposals to management.

• Because Elliott’s focus on short-term profit conflicts with Sumitomo’s long-term redevelopment strategies, we should pay close attention to the way Sumitomo approaches urban redevelopment projects in the future.